Anthony Toupin

Senior Research Analyst - Global Investment Research

The year has been dominated by announcements of astronomical investments in AI, raising the spectre of a speculative bubble in the technology sector. However, our analysis qualifies this risk, as the outlook remains constructive for digital infrastructure giants and semiconductor suppliers. The key for investors will be to remain selective, focusing on financial strength and realistic growth opportunities rather than media buzz.

The year has also been marked by multiple twists and turns in the tech sector, particularly in AI. In January, the announcement of the introduction of a low-cost Chinese AI model, DeepSeek, disrupted the Western ecosystem, raising questions about the real return on investment made by hyperscalers (large cloud companies). While the market initially reacted negatively to this news, the DeepSeek effect was short-lived. The arrival of DeepSeek ultimately proved to be a positive catalyst for the AI theme, consistent with the Jevons paradox, whereby lower development costs will naturally increase the adoption of AI in the long term, as was the case at the end of the 19th century, when the introduction of a more coal-efficient steam engine paradoxically increased the consumption of coal by leading to the widespread adoption of the new generation of steam engines.

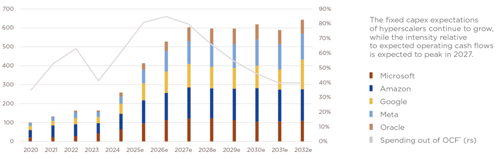

This short-lived fear failed to perturb the upward trajectory of the fixed capex expectations of hyperscalers, which appear to be more concerned about the prospect of losing ground to the competition than making short-term returns on investment. While the market consensus in 2024 was for fixed capex by cloud giants of around $620 billion between 2025 and 2027 (i.e. 12% of their expected revenues over the period), the consensus expectation has now risen to $1.7 trillion, equal to nearly 30% of expected revenues.

Chart 1 — Expected fixed capex per year, by hyperscaler and in relation to operating cash flows (period 2020 – 2032e)

Amount in billions of dollars

*OCF: operating cash flow

Source: Edmond de Rothschild, Bloomberg.

This sharp rise in fixed capex expectations has resulted in a substantial increase in the share prices of AI hardware technology providers, particularly semiconductor stocks. The latter once again posted an impressive performance in 2025, with the SOX, the global index of semiconductor stocks, outperforming the MSCI World by 22% at end-November (+42% versus +20%, in dollars). In addition, the semiconductor sector, which accounted for 2% to 4% of the S&P 500 for 20 years, has in just three years come to claim 14% of the index.

Semiconductor stocks, identified as the immediate beneficiaries of this capital expenditure, thus continue to benefit from the continued increase in spending expectations as “hardware suppliers”, boosting the rise of AI, regardless of the return on investment for hyperscalers in the longer term. Nvidia, the current leader in graphics processors for AI, recently said that it expects fixed AI capex to reach more than $3 trillion per year by 2030, raising questions over “hyper-spending” and, hence, the potential formation of an AI market bubble.

Chart 2 — Weight of semiconductors in the S&P 500 relative to the trend in the sector’s earnings-per-share expectations, against those of the index

Source: Edmond de Rothschild, Bloomberg.

The expenses race is stepping up, and not just among hyperscalers.

This trend has gathered steam recently following announcements of partnerships between several tech giants aimed at developing additional AI data centre capabilities, the common denominator being ChatGPT creator OpenAI.

At the time of writing, OpenAI was apparently committed to financing more than $1.5 trillion in data centre and cloud infrastructure capacity, or 26 GW of AI capacity, in addition to a 10 GW target as part of the Stargate project announced earlier this year. These commitments are nearly four times higher than the peak power consumption of New York City. To put these announcements into context, OpenAI is expected to generate less than $20 billion in revenue in 2026 and has said that it does not expect to be profitable before 2029. Looking beyond these astronomical sums of money, the main fears concern the increasing circularity of the financing. Will OpenAI need to finance purchases of chips by Nvidia, AMD, Broadcom, etc. through financing from Nvidia, AMD, Broadcom, etc. from its own suppliers, or are there other ways for OpenAI to finance these substantial commitments on data centre capacity?