Hervé Prettre

Head of Global Investment Research

The current year has been marked by a significant rise in equity indices, but also by a particular performance with an extreme concentration on a few major stocks. While some factors suggest that the trends observed in 2024 and 2025 could continue in 2026, new opportunities and threats are also likely to arise. Investors with a long-term horizon could take advantage of potential weaknesses to add to their positions.

2025: a profitable but singular year for equities

. In the United States, the S&P 500 (at the time of writing) posted a double-digit performance, driven by a relaxed tariff policy, solid earnings and declining rates. Almost two thirds of the S&P 500’s annual performance in 2025 is tied to the top ten stocks, which also account for nearly two-thirds of the index’s earnings growth, particularly tech stocks exposed to AI. But the driving role of AI and some high valuations raise fears of a speculative bubble at the end of 2025.

. In Europe, the market outperformed considerably at the start of the year, boosted by the ReArmEU Europe defence stimulus plan and the German infrastructure programme, and also by capital outflows from the US market in response to the erratic policies of Donald Trump. This has substantially affected European listed companies, as outflows from a capitalised US market worth $60 trillion to a European market valued at €12 trillion have mathematically had a considerable impact. However, after Trump’s tariff backtracking and exceptional earnings and outlooks for US tech stocks, and with euro strength weighing on European corporate profits, European markets have yet to return to their March 2025 peak, underperforming the US market since the April recovery.

. China, a drag on emerging markets since 2021, has turned out to be a driver in 2025. The Chinese government’s policy on curbing deflation, together with a series of stimulus measures and an easing of relations with the US, has boosted expectations in this market, which is also attractively valued.

. Emerging markets had a significant discount early this year, but this has since shrunk across the board. Once again, this can be

explained by investors seeking assets outside of the US exceptionalism theme and Trump easing tariffs. As a result, emerging markets have posted one of the best performances since the beginning of 2025 among the major economic zones.

What to expect in 2026?

. The US market is still benefiting from favourable winds, including expectations of three to four rate cuts in 2026, the resilience of economic growth (thanks in particular to Trump's tax cuts), the momentum of AI investments, which continue to accelerate, and the prospect of deregulation. However, market valuations have become expensive, the consensus is already highly optimistic, and the country’s AI leadership is set to decline going forward. As such, market players anxiously await the sales outlook for hyperscalers1 and semiconductor companies ahead of each earnings report so that they can determine whether AI momentum is still accelerating or whether the lion’s share of the investment drive is behind us, which has historically been a key sign that a bubble has peaked. A peak in growth expectations is usually expected (as in the past with the normalisation of growth in railway line construction, or the sales of transistors, televisions and fibre optics) but this could not happen until 2026, or even later. AI momentum appears to be holding up for now, but it cannot last forever. In addition, such a restrictive concentration of performance on a very limited number of stocks is traditionally expected to reverse. Which makes it wise at this stage for investors to maintain their tech positions in 2026 while extending their focus to other sectors, such as healthcare or industrials, which are staging a strong recovery and boast more moderate valuations.

. The European market is waiting for a growth driver, which should be reflected either in a weaker euro, stronger domestic growth, or both. Our forex forecasts point to a slight appreciation of the dollar, but not sufficiently, in theory, to boost earnings significantly. Economic growth is expected to be supported by the implementation of the German infrastructure plan but could be undermined by uncertainties over the political future of France. However, as many companies have restructured and are starting from zero-growth earnings estimates in 2025, European earnings could rebound by 10% or more in 2026. This could revive investor appetite in European assets, particularly financials and industrials benefiting from the stimulus plans.

. The Chinese market and emerging markets also remain cheap, although these valuations have increased slightly since early 2025. This momentum could continue, but it will require fresh impetus, because the low valuation argument (the main determinant of their 2025 performance) is less convincing than previously. China’s stimulus policies, and potentially lower deflation, could serve as catalysts.

Volatility spikes are likely, as in April 2025. Early that month, Trump presented a list of tariffs, which were deemed arbitrary and prohibitive. This immediately led to a considerable 12% dip in equities, but this trend quickly came to a halt, underlying the importance of remaining invested in April 2025. Fear-provoking developments are still possible given global fragmentation, Trump’s methods, political risks in Europe, and the overall geopolitical context. For medium- and long-term investors, it has been shown that maintaining investments over time can generate returns on the equity markets.

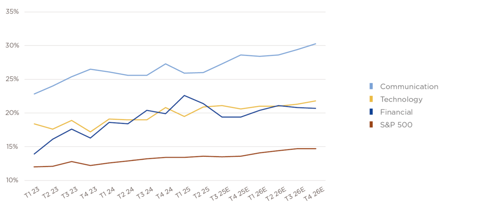

Chart 1 — Expected profit margins for S&P 500 companies and a few sectors

Operating margin as a percentage of revenue, by quarter

Source: Edmond de Rothschild, Bloomberg.

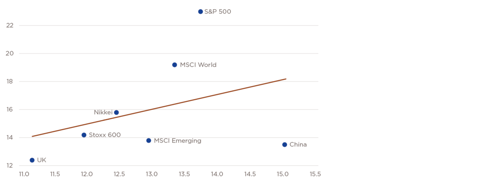

Chart 2 — Estimated earnings growth and P/E 2026

Source: Edmond de Rothschild, Bloomberg.

Which sectors to favour in 2026?

Diversification is fundamental, between sectors with low valuations that look to be stabilising (e.g. healthcare), sectors benefiting from momentum driven by investment flows (e.g. technology), and sectors with solid fundamentals. This is the case for industrials, which are benefiting from European recovery plans, Donald Trump’s determination to re-industrialise, the decline in deflation in China and the dip in global trade risk, and also for financials, through better European growth, the prospect of a capital union in Europe, and deregulation in the United States.

2025 was supposed to be different from 2024. This was not the case in the US, where a few large groups continued to dominate the market, with the markets performing entirely differently in Europe and China. 2026 is expected to be different from 2025, though with similar dynamics. We continue to expect the outperformance (particularly in the US and China) of large groups that are close to the government, able to gain market share and possess greater resources to invest, particularly in AI. In Europe, the fate of large groups will depend more on the euro and global trade. In any case, Trump’s focus on the performance of the S&P 500 together with the low valuation of European and Chinese markets and the level of savings in Europe and China (as well as tax cuts in the US that benefit the wealthiest investors in US equities), could act as safety nets in the event of a major fall in prices.

A host of surprises could also be in store in 2026:

. Will Donald Trump impose new tariffs if China does not follow his injunctions? Will he start a conflict to oust Nicolas Maduro from power in Venezuela?

. Will the future Chairman of the US Federal Reserve be taken seriously by the markets?

. Will the surge in investment in AI continue?

. Will there be peace in Ukraine?

. Will Germany release the promised investments in early 2026?

. Will Jordan Bardella become the prime minister or president of France?

This list is far from complete and many ups and downs are to be expected that could generate concerns and volatility but could also stand as opportunities for the well-informed investor.

1 A hyperscaler is an IT service provider that operates data centres on a very large scale to offer cloud computing and data management services. Hyperscalers are dominant cloud operators including Amazon, Google, Microsoft, and Alibaba.