Rami Boustany

Head of Fixed Income Credit Research - Global Investment Research

Dieter Van de voorde, CAIA, CQF, IFID

Senior Fixed Income Portfolio Manager

Bond credit spreads have fallen over the past three years, prompting us to reassess the attractiveness of this asset class. While low spreads make bond valuations vulnerable to any increase in risk aversion, absolute yields remain above their ten-year historical average, offering attractive carry opportunities, certainly since interest rates remain relatively high in the US and Europe.

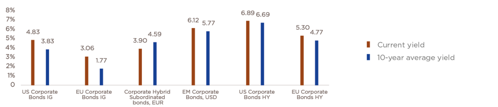

US and European investment grade bonds are yielding 4.83% and 3.06%, respectively, compared with averages of 4.35% and 2.65% over the past five years. The yields on high yield and emerging market corporate bonds currently stand at 20 to 50 basis points below their five-year average but remain above their ten-year average.

Chart 1 — Current yield versus 10-year average yield per bond segment, as a percentage

Source: Edmond de Rothschild, Bloomberg at 07/11/2025.

This level of spreads reflects a stabilisation of default rates at low levels in recent years, with no expectation of any significant increase on a global scale. This is explained by the resilience of the global economy, growth in corporate profits and the relative strength of corporate balance sheets. As inflation moves closer to central bank targets in the US and Europe, following the monetary tightening of the Federal Reserve and the European Central Bank in 2024, government budget deficits and rising sovereign debt increase the risk of steepening yield curves, a factor that could provoke volatility in this asset class.

Investment grade segment

In this segment, the preference is for large companies with a strong competitive position, stable profitability, and the ability to generate strong cash flows. At the same time, we are making selective forays into sectors that are still at the bottom of the economic cycle, with a view to capturing more attractive spreads. For example, some sectors offer attractive yields:

. Leading car manufacturers with strong balance sheets, robust liquidity and credible recovery plans to restore their competitiveness in terms of model range and cost structure.

. Chemical companies with solid credit metrics, diversified businesses and production partially located in regions with lower energy and commodity costs than Europe, such as the US. We remain cautious on credit that risks being downgraded to high yield.

. Telecom companies with a diversified range of services and products, sizeable market shares and stable credit metrics despite high investments.

. Sectors with high but sustainable debt levels thanks to high profitability and good earnings visibility, often guaranteed by favourable regulation or long-term contracts: infrastructure (motorway concessions, airports, telecommunication towers), real estate, utilities (gas and electricity distribution and transmission), electricity generation and renewable energies.

The large European and US systemic banks remain attractive in investment grade, offering high yields despite their large capitalisations. The risk premium reflects a complex capital structure, combined with obligations with bail-in clauses allowing a bail-in without external assistance.

Emerging markets

Emerging market companies are following the general trend of the bond market, with relatively strong credit ratios, though spreads are historically low. This segment can be integrated into portfolios to improve returns and diversification, but higher risk tolerance is required. Due to the economic and political disparities between emerging markets and between emerging markets and developed markets, bond selection needs to be rigorous. The criteria for investment grade companies in developed markets are also valid here, with additional attention to be paid to a few key points:

. Low currency risk or cost structure mainly in local currency tending to depreciate, combined with high revenues in hard currencies.

. The ability to pass on inflation.

. Solid fundamentals independent of any government support.

. Business activities in strategic sectors for their country.

The preferred sectors include:

. State-owned companies monopolising the extraction of raw materials (integrated oil companies, iron ore & gold miners, phosphate) in Latin America, Central Asia or North Africa.

. Utilities, particularly electricity distribution and transmission, benefiting from favourable regulations and solid positions, mainly in the Arabian Peninsula but also in Eastern Europe and Latin America.

. Exporting companies, except in markets where the local currency is appreciating in real terms (Turkey), or large multinationals. These companies operate in cement, aerospace, airlines or port operation.

. Domestic systemic banks.

. Real estate companies with healthy balance sheets in the Gulf countries.

Subordinated hybrid bond segment

This segment also offers carry opportunities but with complex instruments. Their yield is higher than senior bonds (+60 basis points in US dollars and +90 in euros), justified by a higher level of risk:

. These instruments are subordinated, significantly reducing the residual value in the event of default.

. Coupons may be deferred.

. Their effective maturity is uncertain, but issuers have several possible call dates.

Subordinated hybrid bonds are generally issued by companies with a defensive business model, holding monopolistic positions (electricity and gas distribution and transmission), subject to regulation and long-term contracts guaranteeing the recovery of investments and compensation against the volatility of commodities prices in the midstream (pipelines, gas pipelines). They also cover the sectors of electricity generation, renewable energy projects, telecommunications and integrated oil companies with dominant positions in rational competitive environments.

High yield segment

For risk-tolerant investors, exposure to the high yield segment improves portfolio returns. Spreads are also tight, with credit indicators stronger than in the last five years, but balance sheet quality and operational performances are less consistent than in investment grade, calling for rigorous selectivity. In the European high yield segment, the preferred sectors are:

. Automotive Original Equipment Manufacturers (OEMs), faced with high energy costs, a slowdown in electric car sales in Europe, and a loss of market share in China. We are focused on French OEMs that have managed to reduce their costs, reposition their activities and maintain sustainable credit metrics despite the lack of revenue growth.

. Telecommunications, where debt is high. The preference is for companies with better network quality and a strong competitive position on 5G coverage and fibre optic broadband development. We remain cautious on businesses that are struggling to reverse the decline in the number of subscribers.

. Leading companies in fragmented markets, enabling growth through frequent acquisitions of smaller competitors and higher margins thanks to cumulative synergies. These companies operate in the leasing of equipment for construction or mobile electricity generation, waste treatment, or engineering services.

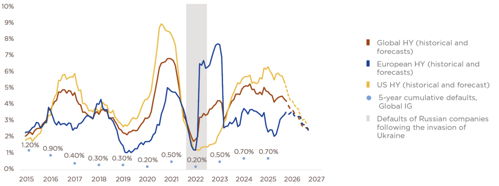

The fixed income asset class contributes to performance through persistently attractive carry. Despite low credit spreads and the risk of steepening of yield curves, risks are mitigated by a contained default rate environment.

Chart 2 — Rolling 12-month default rate for high yield corporates and rolling 5-year cumulative default rate for global IG corporates, as a percentage of the number of issuers

Source: Edmond de Rothschild, Moody’s.